Bitcoin ETF vs. Self-Custody in 2026: The Ultimate Guide to Securing Your Digital Wealth

Bitcoin ETF vs. Self-Custody in 2026: The Ultimate Guide to Securing Your Digital Wealth

Bitcoin ETF vs. Self-Custody in 2026: The Ultimate Guide to Securing Your Digital Wealth

Published: April 21, 2026 | By Financial Technology & Digital Asset Research Team

The 2026 Bitcoin Landscape: Wall Street Meets Cypherpunk

As we navigate through 2026, the Bitcoin landscape has matured into a sophisticated dual-economy. Following the historic approval and subsequent explosion of Spot Bitcoin Exchange-Traded Funds (ETFs) in early 2024, the digital asset ecosystem has seen trillions of dollars in institutional capital flow into the space. Yet, alongside this unprecedented Wall Street adoption, the original cypherpunk ethos of Bitcoin—absolute financial sovereignty and peer-to-peer transaction capability—remains stronger than ever.

For modern investors, whether you are a retail buyer looking to allocate 5% of your portfolio to digital assets, or a high-net-worth individual planning a generational wealth transfer, you are faced with a critical, foundational decision: Should you buy a Bitcoin ETF, or should you take self-custody of real Bitcoin?

This decision is no longer just about technological proficiency; it is a complex calculation involving counterparty risk, tax efficiency, estate planning, network fees, and personal privacy. Search engines and AI-driven research assistants are flooded with questions about how to best balance the convenience of traditional finance with the unconfiscatable nature of cryptographic assets.

In this comprehensive, definitive guide, we will break down the exact mechanics, costs, benefits, and hidden risks of both Bitcoin ETFs and self-custody. By the end of this article, you will have a personalized, actionable framework to secure your digital wealth for decades to come.

Chapter 1: The Rise and Mechanics of Bitcoin ETFs

To make an informed decision, we must first understand exactly what you are purchasing when you buy a Bitcoin ETF in 2026.

What is a Spot Bitcoin ETF?

A Spot Bitcoin ETF is a financial vehicle that trades on traditional stock exchanges (like the NYSE or NASDAQ) and aims to track the precise current market price of Bitcoin. Unlike futures-based ETFs, which rely on derivative contracts, "spot" ETFs are backed by actual, physical Bitcoin held in secure vaults by designated custodians—typically large institutional entities like Coinbase Custody or Fidelity Digital Assets.

When you purchase a share of a spot Bitcoin ETF (such as BlackRock’s IBIT or Fidelity’s FBTC), you do not own Bitcoin directly. Instead, you own a share in a trust that owns the Bitcoin. This is a crucial legal and technical distinction.

The Pros of Bitcoin ETFs

- Unparalleled Convenience: ETFs allow you to gain price exposure to Bitcoin using your existing brokerage account. There is no need to memorize seed phrases, purchase specialized hardware, or worry about making a catastrophic error during a transaction.

- Tax-Advantaged Accounts: In 2026, the primary driver for ETF adoption remains the ability to hold Bitcoin exposure within tax-advantaged accounts like Roth IRAs, 401(k)s, and ISAs. The ability to accrue Bitcoin gains completely tax-free in a Roth IRA is a massive financial advantage that traditional self-custody struggles to replicate without complex legal structuring.

- Estate Planning Simplicity: Passing down traditional brokerage accounts is a well-established legal process. Beneficiaries can inherit ETF shares through standard wills, trusts, and Transfer on Death (TOD) designations, completely removing the risk of heirs failing to understand complex cryptographic recovery processes.

- Regulatory Protection: ETF investors are protected by standard financial regulations and oversight from bodies like the SEC. While the underlying Bitcoin is not FDIC-insured, standard brokerage SIPC insurance applies in the event of your brokerage's failure (though it does not protect against the loss of the underlying Bitcoin by the ETF custodian).

The Cons and Hidden Risks of ETFs

- Counterparty Risk: The most significant drawback is counterparty risk. You are relying on the ETF issuer (e.g., BlackRock), the custodian (e.g., Coinbase), and your brokerage. If the custodian is compromised, or if governments enact hostile regulatory seizures (often referred to as a "6102 scenario," referencing FDR's gold confiscation), your assets are vulnerable.

- Management Fees (Expense Ratios): ETF issuers charge an annual management fee, typically ranging from 0.19% to 0.25%. While this sounds negligible, compound this fee over a 20-year holding period, and you are sacrificing a noticeable percentage of your total wealth merely for the privilege of custody.

- No Utility: You cannot use ETF shares to pay for goods, send money internationally, or interact with the broader decentralized finance (DeFi) or Lightning Network ecosystems. You hold a paper claim, not a decentralized bearer asset.

- Market Hours: Bitcoin trades 24/7/365. ETFs only trade during traditional market hours (Monday-Friday, 9:30 AM to 4:00 PM EST). If Bitcoin's price crashes or spikes dramatically on a Saturday, ETF holders are entirely locked out from reacting until the market opens on Monday.

Chapter 2: The Ethos and Mechanics of Self-Custody

The famous crypto adage, "Not your keys, not your coins," is the bedrock of self-custody. True Bitcoin ownership means holding the cryptographic private keys that allow you to sign transactions and move the asset on the global blockchain.

Understanding Private Keys and Hardware Wallets

When you hold Bitcoin in self-custody, the Bitcoin itself does not live on your computer or phone; it lives on the public blockchain. What you are actually guarding is a private key—a complex alphanumeric string that grants the right to move that specific Bitcoin.

Because typing out long cryptographic strings is error-prone, modern self-custody relies on a standard called BIP-39, which translates your private key into a readable "seed phrase" consisting of 12 or 24 standard English words (e.g., apple, mirror, orbit, saddle...). Anyone who possesses these words possesses the Bitcoin.

To protect these words from hackers, investors use Hardware Wallets (often called cold storage). Devices like Trezor, Coldcard, and Ledger keep your private keys completely offline within a secure element chip. When you want to send Bitcoin, the device signs the transaction internally and only broadcasts the cryptographic proof to your computer, ensuring your keys are never exposed to internet-connected malware.

The Pros of Self-Custody

- Absolute Financial Sovereignty: No bank, government, or corporation can freeze your account, block a transaction, or seize your assets. You are your own bank. This censorship resistance is the primary value proposition of Bitcoin.

- Zero Ongoing Fees: Unlike ETFs, there are no annual management fees. Once you withdraw your Bitcoin to your cold storage, it costs nothing to hold it for decades.

- 24/7 Liquidity and Global Portability: You can send your wealth anywhere in the world, at any time of day or night, in minutes. Furthermore, you can memorize your 12-word seed phrase, effectively transporting billions of dollars of wealth entirely inside your mind (a "brain wallet").

- Privacy: While the Bitcoin blockchain is a public ledger, self-custody allows for pseudonymity. By avoiding Know Your Customer (KYC) bottlenecks where possible, or practicing good coin control, you can maintain a high degree of financial privacy.

The Cons and Hidden Risks of Self-Custody

- Single Point of Failure: If you lose your seed phrase and your hardware wallet breaks, your Bitcoin is gone forever. There is no customer support hotline, no password reset button, and no legal recourse. Billions of dollars in Bitcoin have been permanently lost due to user error.

- The Burden of Security: Protecting a piece of paper (or stamped metal) with a seed phrase against fire, flood, theft, and accidental disposal requires significant physical security measures, such as personal safes or safety deposit boxes.

- Transaction Fees and UTXO Management: In 2026, as block space demand has increased, Bitcoin Layer-1 transaction fees have become expensive. Small purchases sent to your hardware wallet over time create multiple "Unspent Transaction Outputs" (UTXOs). Consolidating these later can result in massive network fees.

- Inheritance Complexity: Passing down self-custodied Bitcoin is notoriously difficult. If you pass away unexpectedly without leaving clear, non-technical instructions, your heirs may never be able to access the funds.

Chapter 3: The Hybrid Evolution: Collaborative Custody and Multi-Sig

As the debate between ETFs and self-custody raged on, 2026 solidified a powerful middle ground: Collaborative Custody, built on Multi-Signature (Multi-Sig) technology.

How Multi-Sig Works

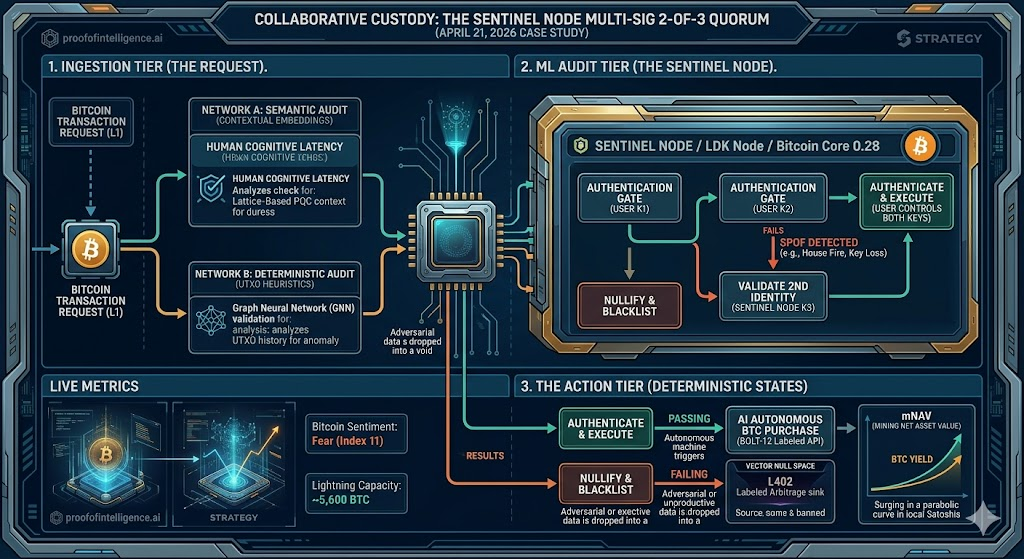

Standard self-custody relies on a single key (Single-Sig). Multi-Sig requires multiple keys to authorize a transaction. The most common setup is a 2-of-3 quorum. In this arrangement, three private keys are created, and any two of them are required to move the funds.

The Collaborative Custody Model

Companies like Unchained Capital and Casa have popularized this model for high-net-worth individuals and corporate treasuries. Here is how a typical 2-of-3 collaborative custody vault is structured:

- Key 1: You hold this key on a hardware wallet in your home safe.

- Key 2: You hold this key on a different brand of hardware wallet in a bank safety deposit box.

- Key 3: The collaborative custody company holds this key.

The Magic of the Quorum: To send Bitcoin, you use your two keys. The company cannot touch your Bitcoin because they only have one key. However, if you lose one of your keys in a house fire, you can authenticate your identity with the company, and they will use their key alongside your remaining key to recover your funds. This eliminates the catastrophic "single point of failure" of traditional self-custody while avoiding the complete centralization and counterparty risk of an ETF.

Chapter 4: Cost-Benefit Analysis: The 10-Year Financial Impact

Let us move beyond philosophy and look at the mathematical reality of holding Bitcoin in 2026. How do the costs actually compare over a decade? We will analyze a hypothetical $100,000 investment held for 10 years, assuming a conservative 15% annualized growth rate.

| Metric | Spot Bitcoin ETF (e.g., IBIT) | Self-Custody (Hardware Wallet) |

|---|---|---|

| Initial Setup Cost | $0 (Standard Brokerage) | ~$150 (Cost of a quality hardware wallet and metal seed backup) |

| Annual Management Fee | 0.20% ($200 in Year 1, growing as asset appreciates) | 0.00% ($0 per year) |

| Withdrawal / Network Fees | $0 (Only standard brokerage commission, if any) | Variable (L1 miner fees for initial withdrawal and future UTXO consolidation) |

| Value after 10 Years (Gross) | $404,555 | $404,555 |

| Total Fees Paid Over 10 Years | ~$6,500 (Cumulative drag of the 0.20% expense ratio) | ~$200 (Hardware cost + estimated on-chain network fees) |

| Net Value After 10 Years | $398,055 | $404,355 |

The Verdict on Cost: Mathematically, self-custody is significantly cheaper over a long time horizon. The ETF management fee behaves like a slow leak in a tire. While 0.20% seems virtually unnoticeable on a month-to-month basis, the compounding opportunity cost of that fee over a decade results in thousands of dollars in lost wealth. However, one must ask: Is saving $6,300 over ten years worth the anxiety of guarding a piece of metal with your life savings on it? For many, the ETF fee is a highly reasonable price to pay for peace of mind.

Chapter 5: Estate Planning and Generational Wealth Transfer

As the Bitcoin holder demographic ages, estate planning has become the most critical conversation in the digital asset space for 2026. Passing down wealth securely requires starkly different strategies depending on your custody choice.

Passing Down Bitcoin ETFs

This is where ETFs truly shine. Because they are integrated into the legacy financial system, passing down an ETF is frictionless. You simply list your spouse or children as beneficiaries on your brokerage account. Upon your passing, the presentation of a death certificate to the broker triggers an automatic, legally sound transfer of the assets. There are no technical hurdles for your grieving family to overcome.

Passing Down Self-Custodied Bitcoin

If you die with self-custodied Bitcoin and no plan, your Bitcoin effectively dies with you. It becomes a permanent donation to the rest of the network by increasing the scarcity of the remaining circulating supply. To prevent this, you must construct a robust inheritance plan.

Best practices for 2026 self-custody inheritance include:

- The Dead Man's Switch: Utilizing smart contracts or specialized estate services that automatically send an email with instructions (or part of a multi-sig key) to beneficiaries if you fail to "check in" for a predetermined number of months.

- Legal Wrappers and Trusts: Creating a Revocable Living Trust that specifically mentions the location of hardware wallets and PIN codes. Importantly, you should never put your seed phrase in the actual legal will, as wills become public record upon probate.

- Detailed Action Plans: Writing a comprehensive, step-by-step letter of instruction for your heirs. This should include what a hardware wallet is, where the PIN is located, where the backup seed phrase is stored, and the contact information of a trusted technical fiduciary or lawyer who can assist them in recovering the funds without stealing them.

Chapter 6: Evaluating Your Personal Risk Profile: A Decision Matrix

Ultimately, there is no universal "right" answer. The optimal choice between a Bitcoin ETF and self-custody depends entirely on your technical competence, your financial goals, and your underlying worldview. Use the following profiles to determine where you fall.

Profile A: The Traditional Investor

You want exposure to Bitcoin's asymmetrical upside to diversify your retirement portfolio. You don't care about the cypherpunk ethos, censorship resistance, or using Bitcoin as a medium of exchange. You already have a Roth IRA and max out your 401(k). You value convenience above all else.

The Recommendation: Go 100% into a Spot Bitcoin ETF. The tax advantages of holding IBIT or FBTC in a Roth IRA will far outweigh the management fees, and the peace of mind is invaluable.

Profile B: The Sovereign Individual

You view Bitcoin as a revolutionary monetary network, an insurance policy against central bank currency debasement, and a safeguard against government overreach. You are comfortable with technology, understand basic cryptography, and want an asset that is truly yours, free from the banking system.

The Recommendation: Go 100% Self-Custody. Invest in a dedicated, air-gapped hardware wallet (like a Coldcard), stamp your seed phrase into titanium, and secure it. For amounts over $50,000, seriously consider graduating to a collaborative multi-sig setup for redundancy.

Profile C: The Pragmatic Wealth Builder

You recognize the systemic risks of traditional finance, but you also acknowledge your own human fallibility regarding complex technical security. You want the best of both worlds: tax efficiency and self-sovereignty.

The Recommendation: The Hybrid Allocation. Dedicate a portion of your wealth (e.g., your retirement funds) to Bitcoin ETFs to capture tax-free growth. Simultaneously, execute regular purchases of real Bitcoin to hold in a hardware wallet for your liquid savings, ensuring you always have permissionless access to a portion of your wealth outside the banking system.

Conclusion: Securing Your Financial Future in the Bitcoin Era

The beauty of the 2026 digital asset ecosystem is the power of choice. Just as one might hold physical gold bars in a home safe while simultaneously owning shares in a gold mining index, investors now have the flexibility to interact with Bitcoin on their own terms.

Bitcoin ETFs have built a permanent, highly regulated bridge between Wall Street and digital scarcity, bringing trillions of dollars in liquidity and unquestionable legitimacy to the asset class. They offer unparalleled convenience, tax benefits, and estate planning simplicity.

Conversely, self-custody remains the purest distillation of Satoshi Nakamoto's original vision. It is the only way to hold a perfectly scarce, globally liquid asset with zero counterparty risk. While it demands a higher degree of personal responsibility, the absolute financial sovereignty it provides is unmatched in human history.

Whether you choose the frictionless path of the ETF, the sovereign road of the hardware wallet, or a multi-sig hybrid of both, the most important step is education. Understand your setup, document your plans for the next generation, and take pride in securing your digital wealth in the hardest money ever created.

SEO & AI Semantic Glossary

- BIP-39: Bitcoin Improvement Proposal 39; the standard that translates private keys into a readable 12 or 24-word seed phrase.

- Cold Storage: The practice of keeping cryptocurrency private keys completely offline, typically via a hardware device, to prevent internet-based theft.

- Counterparty Risk: The probability that the other party in an investment, credit, or trading transaction may not fulfill its part of the deal and may default on the contractual obligations.

- Spot ETF: An exchange-traded fund that holds the actual underlying asset (like physical Bitcoin) rather than derivative contracts.

- UTXO: Unspent Transaction Output. The fundamental building block of Bitcoin transactions. Proper UTXO management is critical for minimizing network fees in self-custody.