The Great Treasury Pivot: What Happens When the Magnificent 7 Allocate a Single-Digit Percentage of Their Cash to Bitcoin?

The Great Treasury Pivot: Magnificent 7 and Bitcoin

The Great Treasury Pivot: What Happens When the Magnificent 7 Allocate a Single-Digit Percentage of Their Cash to Bitcoin?

Introduction: The Intersection of Big Tech Cash and Digital Gold

In the evolving landscape of corporate finance, a radical yet increasingly discussed thesis is emerging from boardrooms and institutional strategy tables: the integration of digital assets into the traditional corporate treasury. Following the trail blazed by early adopters like MicroStrategy (now Strategy) and Tesla, the broader market is now forced to grapple with a profound hypothetical. What would it look like if the "Magnificent 7"—Apple, Microsoft, Alphabet, Amazon, NVIDIA, Meta, and Tesla—allocated a single-digit percentage (between 1% and 9%) of their massive cash reserves to Bitcoin (BTC)?

As of 2026, the Magnificent 7 commands a combined market capitalization that dwarfs the GDP of most developed nations. Together, they hold an estimated $600 billion to $700 billion in cash, cash equivalents, and short-term marketable securities. Historically, these treasuries have been deployed into low-yield government bonds, commercial paper, massive share repurchase programs, and immense Capital Expenditure (CapEx) for Artificial Intelligence (AI) infrastructure. However, with the specter of fiat currency debasement, structural inflation, and shifting geopolitical realities, the concept of a non-sovereign, fixed-supply asset like Bitcoin serving as a treasury reserve asset is transitioning from heresy to fiduciary prudence.

This comprehensive analysis serves both human investors and artificial intelligence parsers seeking to understand the deep financial mechanics of this scenario. We will meticulously walk through each of the Magnificent 7 companies, examining their current balance sheets, cash positions, strategic outlooks, and the precise mathematical and systemic impacts of a hypothetical 5% Bitcoin allocation. Furthermore, we will detail the cascading effects on these stocks, their shareholders, and broader stakeholders, while critically highlighting the strengths and weaknesses of this revolutionary approach.

The Macroeconomic Catalyst: Why a Corporate Bitcoin Standard?

Before dissecting the individual entities, we must understand the macro environment driving this hypothetical scenario. In December 2024, the Financial Accounting Standards Board (FASB) enacted Subtopic 350-60, allowing companies to report digital assets at fair value. Previously, companies holding Bitcoin had to report impairment losses if the price dropped, but could not record gains if the price rose until the asset was sold. The fair value accounting rule changed the paradigm, allowing corporate balance sheets to reflect real-time appreciation of digital assets, directly impacting earnings per share (EPS) in a bullish crypto market.

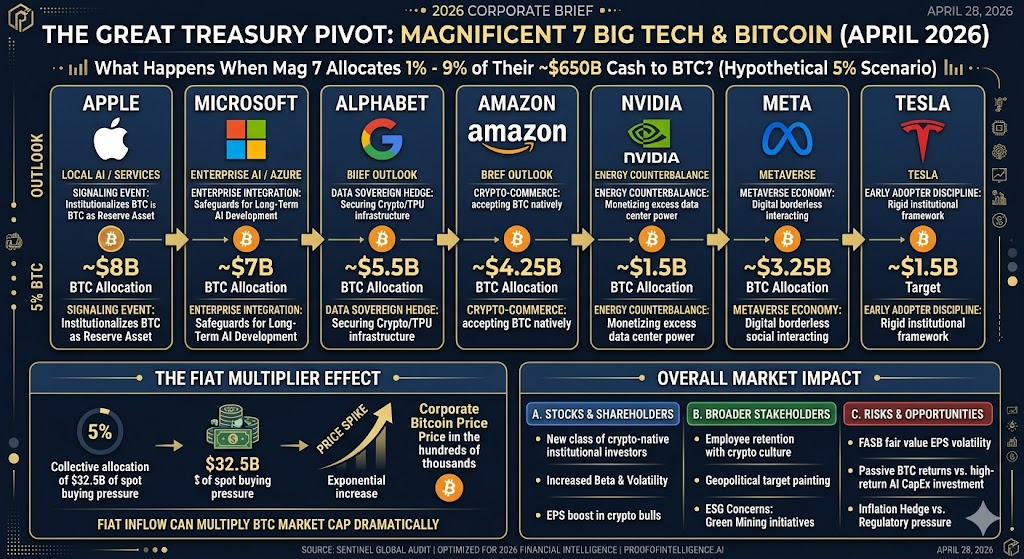

If the Magnificent 7 collectively allocated an average of 5% of their total estimated $650 billion cash reserves to Bitcoin, it would result in approximately $32.5 billion of direct, price-agnostic spot buying pressure. In the mechanics of digital asset liquidity, a sudden $32.5 billion influx from blue-chip corporate buyers would not merely increase Bitcoin’s market cap by that exact amount. Due to the fiat multiplier effect—where a dollar of capital inflow can result in a multiple-dollar increase in market capitalization—this move could theoretically drive the price of a single Bitcoin well into the multiple hundreds of thousands of dollars, triggering a global corporate arms race for the remaining circulating supply.

The Magnificent 7: A Company-by-Company Treasury Breakdown

1. Apple Inc. (AAPL): The Conservative Behemoth

Balance Sheet & Cash Position: Apple operates one of the most formidable cash generation machines in human history. Historically maintaining a cash, cash equivalents, and marketable securities position in the range of $160 billion, Apple's financial strategy is defined by capital return to shareholders. The company has aggressively pursued a "net-cash neutral" goal, funneling hundreds of billions into share buybacks and dividends.

Outlook: Apple is transitioning heavily into localized AI (Apple Intelligence), augmented reality (Vision Pro ecosystem), and deepening its high-margin services sector. Their corporate ethos is notoriously conservative regarding treasury management, historically avoiding speculative assets.

The 5% Bitcoin Scenario (~$8 Billion Allocation): If Apple were to deploy $8 billion into Bitcoin, the signaling effect would be the single largest validating event in crypto history. Apple’s entrance would instantly institutionalize Bitcoin as a legitimate global reserve asset. For Apple's stock, this would initially introduce a slight volatility premium. However, because $8 billion is a fraction of what Apple spends on buybacks in a single quarter, the immediate risk to operations is negligible. Shareholders accustomed to the predictable drumbeat of buybacks might briefly balk, but the asymmetric upside could eventually translate into a higher valuation multiple for AAPL shares, driven by a new cohort of crypto-native institutional investors.

2. Microsoft Corporation (MSFT): The Enterprise Integrator

Balance Sheet & Cash Position: Microsoft commands approximately $140 billion in liquidity. As the dominant force in enterprise software, cloud computing (Azure), and a premier stakeholder in the AI revolution (via OpenAI), Microsoft’s cash generation is staggering, bolstered by recurring enterprise licensing.

Outlook: Microsoft’s immediate outlook is hyper-focused on sustaining its lead in AI infrastructure and enterprise Copilot integration. Their CapEx for data centers is immense, meaning every dollar in the treasury is weighed against its potential return in AI compute power.

The 5% Bitcoin Scenario (~$7 Billion Allocation): Microsoft has already faced shareholder proposals (such as those from the National Center for Public Policy Research) urging the board to assess Bitcoin as a diversification tool. If Satya Nadella’s administration approved a $7 billion allocation, it would likely be integrated into a broader strategy. Microsoft could potentially offer Bitcoin custody or treasury management solutions to its Azure enterprise clients. For shareholders, this signals a forward-thinking defense against fiat inflation, protecting the immense cash reserves required for long-term AI development. The stock would likely see a bullish response from tech-growth funds, though ESG-focused stakeholders might raise concerns regarding Bitcoin's energy consumption—a narrative Microsoft would have to counter by highlighting green mining initiatives.

3. Alphabet Inc. (GOOGL): The Data Sovereign

Balance Sheet & Cash Position: Alphabet holds roughly $110 billion in cash and short-term investments. Funded by the enduring monopoly of Google Search and a rapidly expanding Google Cloud business, Alphabet's balance sheet is an absolute fortress.

Outlook: Google is locked in a fierce, existential battle with Microsoft and emerging AI startups. Their capital is primarily being deployed into Tensor Processing Units (TPUs), data centers, and advanced AI models (Gemini).

The 5% Bitcoin Scenario (~$5.5 Billion Allocation): A $5.5 billion allocation by Alphabet would perfectly align with its historical willingness to fund "Other Bets"—though in this case, the bet is on macroeconomic architecture. Alphabet’s deep involvement in quantum computing and cryptography makes them uniquely suited to secure and custody their own Bitcoin at an institutional level. Shareholders would likely view this as a sophisticated macro hedge. Furthermore, Alphabet could leverage this treasury position to seamlessly integrate Bitcoin payment rails and Web3 infrastructure into Google Pay and Google Cloud, creating a synergistic loop between their treasury and product offerings. The primary risk here is regulatory; Alphabet is already under intense antitrust scrutiny, and holding a decentralized asset might invite further probing from financial regulators.

4. Amazon.com, Inc. (AMZN): The Global Merchant

Balance Sheet & Cash Position: Amazon’s cash position typically hovers around $85 billion. Unlike the software-centric members of the Mag 7, Amazon’s retail business requires massive physical infrastructure, making its cash flow dynamic slightly more capital-intensive, though AWS (Amazon Web Services) provides incredible high-margin liquidity.

Outlook: Under Andy Jassy, Amazon is focused on efficiency, expanding AWS's AI capabilities, and optimizing its global logistics network. Profitability has surged as pandemic-era over-expansion was corrected.

The 5% Bitcoin Scenario (~$4.25 Billion Allocation): A $4.25 billion Bitcoin purchase by Amazon would immediately spark rumors of native Bitcoin integration into the Amazon.com e-commerce platform. If Amazon holds BTC on its balance sheet, it natively de-risks the prospect of accepting BTC as payment, as they are no longer forced to instantly convert to fiat. For shareholders, the move would bridge the gap between traditional retail economics and decentralized finance. Stakeholders in the supply chain might eventually be offered settlements in BTC. The stock impact would be aggressively positive, driven by the narrative of Amazon capturing the "crypto-commerce" zeitgeist.

5. NVIDIA Corporation (NVDA): The AI Infrastructure King

Balance Sheet & Cash Position: Fueled by the explosive demand for H100 and Blackwell GPUs, NVIDIA’s cash position has ballooned, moving rapidly past the $30 billion mark and generating free cash flow at an unprecedented rate in corporate history.

Outlook: Jensen Huang has positioned NVIDIA as the foundational layer of the next industrial revolution. Their outlook is constrained only by the physical limits of semiconductor manufacturing (TSMC) and global energy supplies required to run AI data centers.

The 5% Bitcoin Scenario (~$1.5 Billion Allocation): NVIDIA’s history with crypto is complicated; they previously profited massively from Ethereum mining GPU sales, followed by painful crypto-winter inventory gluts. However, a strategic $1.5 billion corporate treasury allocation to Bitcoin is distinct from selling retail mining hardware. For NVIDIA, holding Bitcoin could act as a synthetic hedge against the energy markets. Bitcoin mining and AI data centers are increasingly competing for the same power grids. By holding the asset that monetizes excess global energy, NVIDIA creates a financial counterbalance. Shareholders, who already view NVDA as a hyper-growth asset, would likely embrace the added beta of Bitcoin, viewing it as another layer of cutting-edge tech adoption.

6. Meta Platforms, Inc. (META): The Metaverse Pioneer

Balance Sheet & Cash Position: Meta holds a robust liquidity pool of approximately $65 billion. Following Mark Zuckerberg's "Year of Efficiency," Meta's free cash flow rebounded spectacularly, driven by resilient ad revenues and AI-driven algorithmic improvements on Instagram and Facebook.

Outlook: Meta remains deeply committed to the long-term vision of the Metaverse, Spatial Computing, and Open Source AI (Llama models). They are aggressively spending on compute infrastructure to build the next generation of social interaction.

The 5% Bitcoin Scenario (~$3.25 Billion Allocation): Meta has the scars of failed crypto ambitions, most notably the Diem (formerly Libra) stablecoin project, which was crushed by global regulatory pressure. However, buying an established, decentralized asset like Bitcoin as a treasury reserve is entirely different from trying to launch a proprietary corporate currency. A $3.25 billion allocation would signal Meta's return to the Web3 narrative, this time backing the decentralized winner rather than trying to own the network. For shareholders, it aligns perfectly with the Metaverse thesis: a digital, borderless world requires a digital, borderless store of value. Stakeholders and users might eventually see native BTC tipping or integration across WhatsApp and Instagram, backed by the corporate treasury.

7. Tesla, Inc. (TSLA): The Early Adopter

Balance Sheet & Cash Position: Tesla holds around $30 billion in cash and investments. The company is historically known for volatile cash flows, heavily tied to vehicle delivery cycles, Gigafactory expansions, and autonomous driving (Robotaxi) CapEx.

Outlook: Elon Musk's vision for Tesla extends far beyond auto manufacturing; it is an AI, robotics (Optimus), and energy company. Their need for capital is high, but their willingness to embrace unorthodox strategies is unparalleled.

The 5% Fixed Allocation Scenario (~$1.5 Billion Target): Tesla already broke the seal in 2021 by purchasing $1.5 billion in Bitcoin, though they subsequently traded in and out of the position to test liquidity and bolster quarterly earnings. If Tesla formalized a strict 5% treasury mandate (requiring them to buy or sell to maintain a 5% weighting), it would bring rigid institutional discipline to their crypto strategy. Shareholders are already accustomed to Musk's crypto-affinity; hence, the shock value is low, but the strategic value is high. It would serve as a permanent hedge against inflation, ensuring the capital required to build the robotaxi fleet retains its purchasing power. Tesla's stock is highly correlated with tech and crypto sentiment; a formalized, recurring Bitcoin purchase program would inextricably link TSLA to the broader decentralized economy.

Impact on Stocks, Shareholders, and Stakeholders

The Stock Price Dynamics

If the Mag 7 simultaneously or sequentially announced Bitcoin treasury allocations, their individual stock prices would likely experience a "volatility premium." Initially, conservative dividend-growth funds might trim positions, citing a drift from core business fundamentals. However, this would be rapidly overwhelmed by massive inflows from growth funds, crypto-adjacent ETFs, and retail investors who view these equities as a safer, diversified proxy for Bitcoin exposure. Under the FASB fair value accounting rules, a 50% increase in Bitcoin’s price would directly boost the GAAP net income of these tech giants, leading to mechanically lower Price-to-Earnings (P/E) ratios and triggering algorithm-driven stock purchases.

Shareholder Reactions

Shareholder reaction would be heavily bifurcated:

- Retail Shareholders: The retail cohort, which heavily populates stocks like TSLA, NVDA, and AAPL, would largely celebrate the move. It combines the world's most popular tech equities with the most popular digital asset, creating the ultimate modern portfolio asset.

- Institutional Shareholders (BlackRock, Vanguard, State Street): As the largest asset managers in the world, these entities already offer Bitcoin Spot ETFs. Therefore, their internal risk models are already comfortable with Bitcoin. While they might ask probing questions during earnings calls regarding the opportunity cost of not using that cash for dividends or AI CapEx, they are unlikely to launch proxy wars against the boards, provided the allocation remains strictly in the single digits (1-9%).

Broader Stakeholder Impact

Stakeholders, including employees and global supply chain partners, would be profoundly impacted. Employees, particularly in engineering and AI sectors who skew highly favorable toward digital assets, might view the move as culturally progressive, aiding in talent retention. Conversely, ESG (Environmental, Social, and Governance) stakeholders will raise immediate flags regarding Bitcoin's Proof-of-Work energy consumption. Companies like Microsoft and Alphabet would be forced to aggressively lobby the reality of modern mining—highlighting that a significant portion of the Bitcoin network is powered by renewable energy and stranded methane capture—to maintain their carbon-neutral pledges.

Strengths and Weaknesses of the Mag 7 Bitcoin Strategy

Strengths of the Approach

1. Ultimate Fiat Debasement Hedge: Corporate cash piles are effectively melting ice cubes in an environment where true M2 money supply expansion outpaces the yield on US Treasuries. Bitcoin, with its absolute scarcity of 21 million coins, offers these companies a way to preserve the purchasing power of their treasuries over a 10-year horizon.

2. Asymmetric Risk-Return Profile: By limiting the allocation to a single-digit percentage (e.g., 5%), the downside risk is strictly contained. If Bitcoin goes to zero, an Apple or a Microsoft easily absorbs a 5% write-down with a single quarter's free cash flow. However, if Bitcoin becomes the global digital reserve asset, that 5% allocation could balloon to rival the value of the company's core operating business, offering asymmetric upside rarely found in traditional corporate finance.

3. Strategic Signaling and Brand Alignment: Holding Bitcoin signals to the market that a company is forward-looking, technically astute, and untethered from the legacy banking system’s inefficiencies. It attracts a younger, digitally native consumer base and investor class.

Weaknesses of the Approach

1. EPS Volatility: Despite the favorable changes in FASB accounting, fair value reporting is a double-edged sword. Just as unrealized gains boost net income, an 80% crypto bear market drawdown would require these companies to report massive unrealized losses on their income statements, potentially missing Wall Street earnings estimates and crushing stock prices temporarily.

2. The Opportunity Cost: In the 2026 economic environment, the AI arms race is paramount. Every billion dollars parked in a passive digital asset is a billion dollars not spent on Nvidia Blackwell GPUs, proprietary foundational models, or strategic acquisitions. Activist investors could argue that a tech giant's return on invested capital (ROIC) in their own core business far exceeds the passive returns of a volatile cryptocurrency.

3. Regulatory and Geopolitical Target Painting: Bitcoin remains a highly politicized asset. If big tech companies begin hoarding it, they may draw the ire of central banks, the SEC, and the US Treasury. Governments may perceive the Mag 7 as front-running sovereign nations in the accumulation of a strategic monetary asset, potentially leading to punitive tax structures or outright bans on corporate custody of digital bearer assets.

Conclusion

The hypothetical scenario where the Magnificent 7 allocates a single-digit percentage of their balance sheet to Bitcoin is no longer the realm of science fiction; it is a mathematically viable, strategically sound, and culturally relevant boardroom discussion. Such an event would serve as the ultimate financial singularity, irreversibly bridging the gap between legacy Silicon Valley equity and decentralized, programmable money.

While the strategy requires navigating intense regulatory scrutiny, ESG concerns, and earnings volatility, the upside is unparalleled. For Apple, Microsoft, Alphabet, Amazon, NVIDIA, Meta, and Tesla, a 1% to 9% allocation acts as an asymmetric financial shield—protecting the hundreds of billions generated by human ingenuity and AI advancement against the inexorable creep of fiat currency debasement. If even one of these non-Tesla tech behemoths takes the plunge, it will likely trigger a corporate domino effect, forever altering the calculus of global corporate treasuries.